In 2019, Calla Property won an award for innovation due to its unique property valuation strategy. The valuations that your lender uses to work out how much you can borrow, is not an exact science and is very difficult for the borrower to contest. While there are many benefits to investing in new property, there is a risk if the property isn't registered and we are constantly working to mitigate all risks to our investors.

Residential property valuation is based on using sales data of properties previously sold of a similar type (lot size, house size, aspect, age, condition) in a comparable location in the previous 6 months. Valuations can vary dramatically for exactly the same property for a number of reasons:

1. TYPE OF BUYER

Owner occupier or Investor – the lender apportions increased risk of default to an investor and provides instructions to the Valuer to use certain types of sales evidence or criteria that reduces their valuation. The Property Industry Body has been arguing with the banking regulator about this issue for many years.

2. LOAN TO VALUE RATIO (LVR)

Whether the client has an LVR of 80% or more and requires mortgage insurance. The greater the LVR, the higher the risk to the lender.

3. THE MORTGAGE INSURER'S LOAN EXPOSURE TO A SUBURB

Valuation is a subjective opinion and not an exact science. This subjectivity has been tested in court and a variance of up to 15% have been accepted as reasonable, although typically within 10% has been deemed acceptable in residential valuations, this provides a buffer for any negligence that may occur in determining value. There are many instances where two Valuers have completely different opinions of value on the same property. Some examples are on the table below.

4. RELEVANCE OF DATA

When the property market is in an upswing mode, Valuers are relying on data that can be 6-12 months old and the market has increased in price since that point in time.

5. THE LENDER

Each lender has preferred valuers. Some of the Lenders choose more conservative Valuers to reduce their risk profile.

6. MARKET VALUATION DEFINITIONS

Market Valuation:

The Valuers opinion of what the property should sell for based on a reasonable selling period in an arm’s length transaction, without any pressure, i.e. when you sell via a real estate agent.

Mortgage Security Valuation:

The Valuer’s opinion of a value that the property should sell for in the event of a default by the client. In these instances, the bank needs to sell the property in a shorter timeframe to recover their loan, i.e. a Mortgagee in Possession Sale. Keep in mind that the lender isn't interested in making a profit from the sale, rather removing the default property from their balance sheet to deliver greater shareholder value.

Sales Evidence:

When it comes to new house and land being valued, we regularly see that the Valuers do not necessarily abide by their own industry body regulations. They tend to use sales evidence that reduces that opinion of value. The sales evidence utilised in the valuation report should ideally:

• Include a minimum of three settled relevant sales.

• Include sales within six months of the date of valuation.

• Include sales within 15% (plus or minus) of the assessed market value.

• Include sales of a similar type, location, age, condition, size of home.

• For new properties that form part of a development incorporating common areas and/or shared facilities (such as strata title, community title, plan of subdivision, etc.) a minimum of three settled re-sales from within the subject group and/or external to the development are to be provided.

• For vacant land and/or new house and land properties situated within a new residential estate; a minimum of three settled re-sales from within the subject subdivision and/or re-sales external to the subject subdivision are to be provided.

The Difference Between Market Valuation And Mortgage Security Valuation Is That A Mortgage Security Valuation Assumes A Forced Sale:

When the lender arranges a valuation, they do not obtain a market valuation, they instead obtain a mortgage security valuation.

When A Detailed Review Of The Valuation Of A New House And Land Package Is Undertaken, These Are The Points That Will Be Commonly Seen In The Details Of The Various Sales Evidence The Valuer Has Relied On To Form Their Opinion:

• Second hand property anywhere from 3-40 years old compared to new;

• Often in inferior locations;

• Older estates with inferior street appeal – no render, no feature architecture, poor landscaping;

• Smaller homes;

• Markedly inferior level of fixtures and fittings – bathrooms and kitchens; and,

• Not located in the same estate as the subject property being valued.

Some valuers use sales evidence which is irrelevant and does not compare apples with apples. Furthermore, they are asked to disregard market valuation and consider the forced sale valuation in the event of a default instead. This is the reason why bank valuations in many cases can be 5% under the purchase price and in some cases even more. This is one of the major reasons why we see such discrepancy between valuations.

Valuers Are Personally Liable

In addition, the Valuers in many cases are contractors and hold their own professional indemnity insurance that makes them personally liable for the advice they provide. Since 2007 several Valuers in QLD have been sued for damages by the banks over valuations that didn’t protect the banks during the GFC property downturn. When this is factored in along with the fact that valuers are personally liable for potential losses that the lender may incur due to a loan and reliance on a valuation, it’s no wonder why many residential Valuers, earning only $150 to complete a valuation within 1 to 2 hours tend to be very conservative.

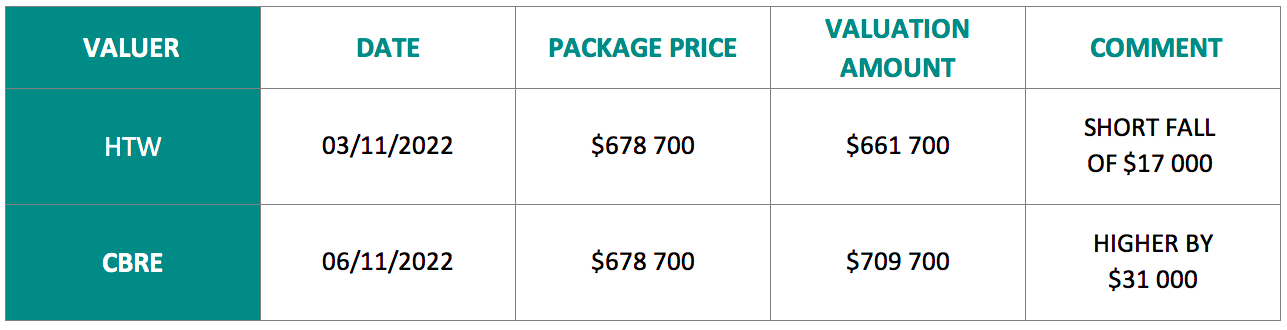

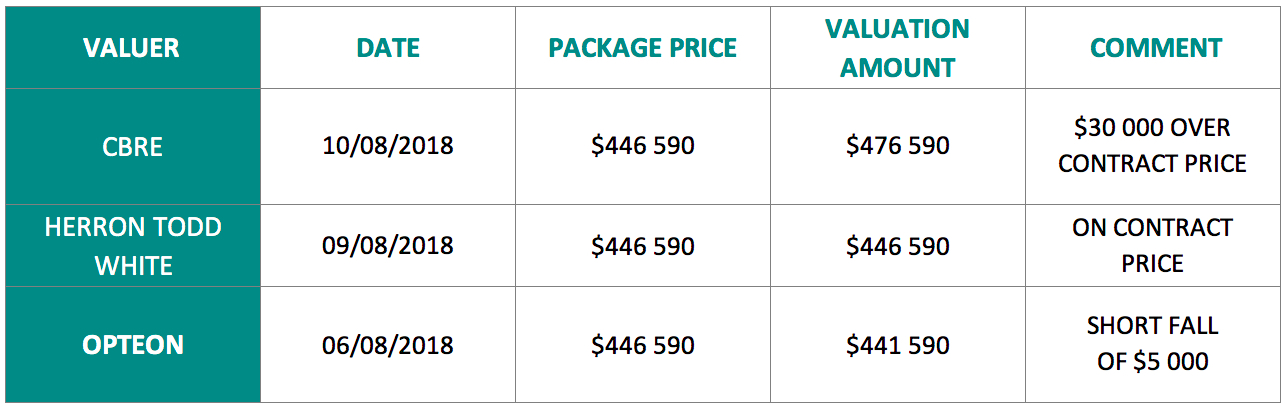

Valuation Differential Examples

The table below shows the discrepancies between different Valuers at different firms valuing the same house and land package with exactly the same evidence available to them. This illustrates that there can be considerable discrepancies in valuations of the same property and the borrower has little to no recourse.